Newsletter | Your Monthly Finance Tips

Monthly Finance tips - April 26

- Details

With the next Reserve Bank decision on May 5 approaching, borrowers are reassessing their position. Here are four trends shaping rates, property prices and your options right now:

With the next Reserve Bank decision on May 5 approaching, borrowers are reassessing their position. Here are four trends shaping rates, property prices and your options right now:

- The refinancing question more borrowers are asking

- How to get more value from your offset account

- Why property prices haven't been falling

- A realistic path from renting to owning

Scroll down for all the stories.

Call me now on: 0402408944

How to stay ahead as rates move higher

Between the Middle East conflict, rising prices and two rate increases this year, many households are feeling the squeeze.

That’s why a lot of borrowers are reviewing their loan, not just riding it out.

Refinancing can help you:

- secure a more competitive rate.

- restructure your loan to suit current conditions.

- improve cash flow.

But timing is the tricky part. Refinance now or wait?

Refinance now or wait?

Refinancing now could mean reducing repayments sooner and getting ahead of further rate rises.

Waiting could mean accessing better rates if markets settle and avoiding switching costs too early.

There’s no perfect moment – it depends on your situation, not just the market.

Where to start

The key is understanding what your current loan looks like compared to what’s available now.

I can help you review your rate, compare options and decide whether acting now or waiting makes more sense for you.

Want to see if you could be paying less?

Your offset could be doing more

As rates rise, offset accounts are becoming more important than many people realise.

That’s because an offset account reduces the interest charged on your loan.

If, say, you have $700,000 outstanding on your loan and $40,000 in offset, you pay interest on only $660,000 (i.e. $700k minus $40k).

This is a hypothetical example – your situation may differ – that shows the power of offset.

As rates rise, the benefit compounds

As rates rise, the interest saved on that hypothetical $40,000 increases.

That means:

- stronger savings without changing your repayments.

- faster loan reduction over time.

- better use of your cash than standard savings.

Making it work properly

Not all offset setups are equal.

Things like account structure, cash flow and loan features can make a big difference.

Contact me if you want help reviewing how your offset is set up and whether it’s working as effectively as it could in the current environment.

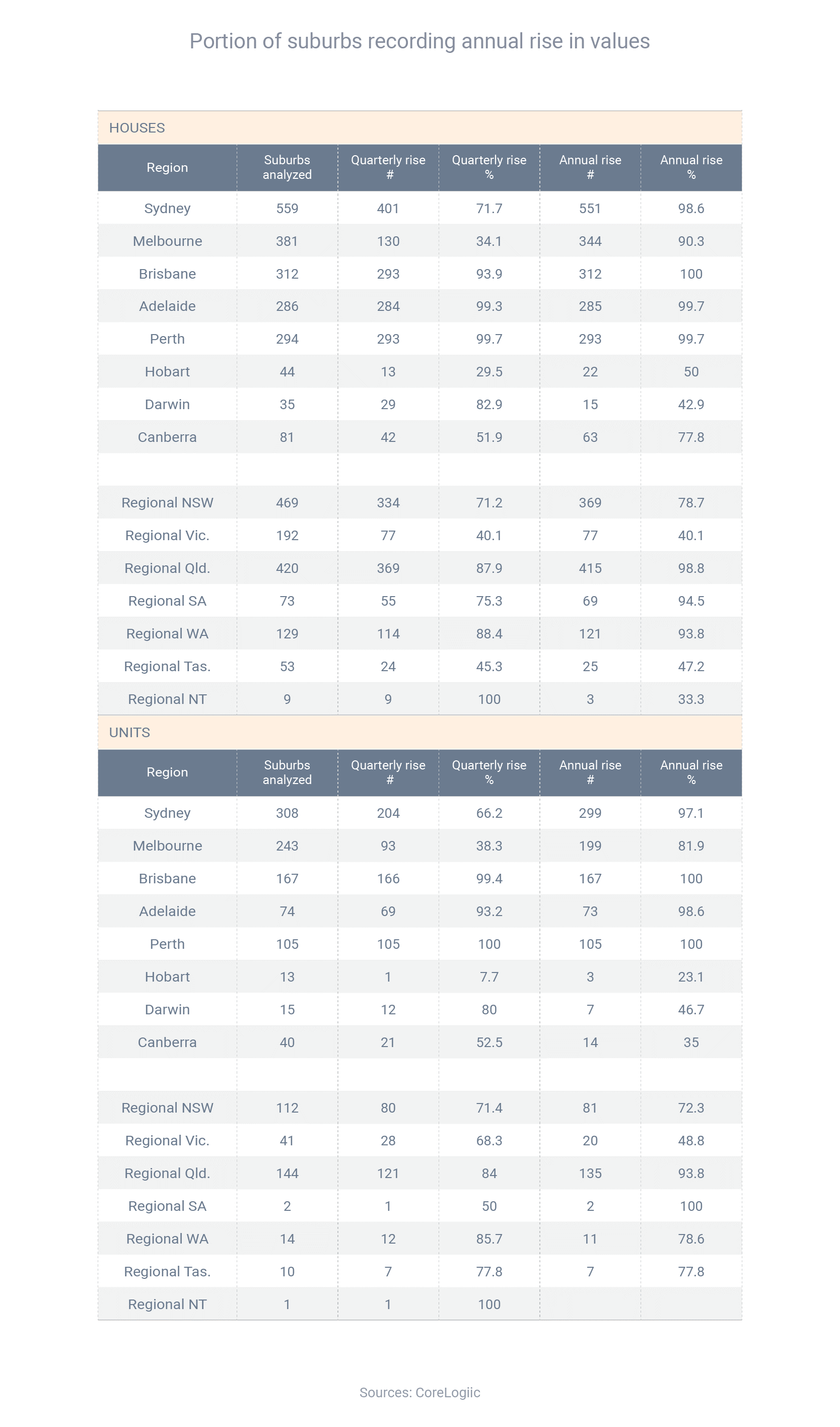

What's really driving property prices

Rising rates haven’t automatically led to falling property prices – and supply is a big reason why.

It’s easy to assume higher rates mean lower prices.

But the data tells a more complex story.

What’s happening now

- National prices rose 0.7% in March (source: Cotality).

- New listings increased 3.8% month-on-month (SQM Research).

- But total listings are still 6.7% lower than a year ago.

That means supply is improving slightly – but still tight overall. The bigger constraint

The bigger constraint

New construction isn’t keeping up.

Master Builders Australia has lowered its forecast for the amount of homes built over the five-year period of the National Housing Accord.

The reason? Labour shortages and cost pressures are slowing supply.

Property prices are being supported by:

- limited housing supply.

- ongoing population growth.

- constrained construction.

So while growth may slow, a broad price decline isn’t guaranteed.

I can help you assess what this means for your borrowing power and whether now is the right time to act.

Rental affordability hits new low

Rents are rising faster than wages. That’s making the path to buying harder – but not impossible.

Rental affordability is now at its lowest level since at least 2008, according to realestate.com.au.

That’s putting pressure on renters trying to save. Why it feels harder

Why it feels harder

Many people are juggling rising rents, higher living costs, elevated property prices and rising interest rates.

It’s a tough combination.

That’s why many buyers are adjusting their approach, rather than waiting for perfect conditions.

That could mean buying a more affordable property, looking at different locations, exploring strategies like rentvesting or using government support schemes where eligible.

The shift that changes timelines

The biggest shift is moving from ‘just waiting’ to understanding what’s possible now.

Even if you’re not ready yet, knowing your borrowing capacity and options can change your timeline.

Reach out if you’d like me to help you map out a realistic path based on your income, savings and goals.

I am a Mortgage Broker with over 30 years experience, I can help first home buyers buy their 1st home, home buyers buy their second, third or fourth home, investment property investors and people who want to build a home.

Based in Victoria Point, I have helped clients all over Australia purchase a home including Gold Coast, Brisbane, Cleveland, Redland Bay, Thornlands, Thorneside, Ormiston, Alexandra Hills, Mt Cotton, Victoria Point, Wellington Point, Birkdale, Shailer Park and the greater Logan area.

Monthly Finance tips - March 26

- Details

From interest rate uncertainty to new ways first home buyers are entering the market, several shifts are reshaping property decisions. These four trends could influence your next move.

From interest rate uncertainty to new ways first home buyers are entering the market, several shifts are reshaping property decisions. These four trends could influence your next move.

- Rate rise reshapes the market

- How the 5% Deposit Scheme is changing buying

- Fixed or variable – which is right for you?

- Building a home is back on the radar

Find out more below.

Call me now on: 0402 408944

Monthly Finance tips - January 26

- Details

Welcome back and happy new year. The market didn’t stay quiet over summer, and with lending rules, investor activity and affordability shifting, it’s worth getting across what’s happening early.

Welcome back and happy new year. The market didn’t stay quiet over summer, and with lending rules, investor activity and affordability shifting, it’s worth getting across what’s happening early.

- Investors claim biggest lending share since 2016

- Affordable homes pull ahead on price growth

- The investing shifts that matter most in 2026

- Mortgage stress eases – but buffers still matter.

Keep reading for all the news.

Call me now on 0402 408944

Monthly Finance tips - February 26

- Details

It’s shaping up to be a decisive start to the year. Borrowing is rising, repayments are shifting and competition isn’t easing. Here’s what’s catching my eye:

It’s shaping up to be a decisive start to the year. Borrowing is rising, repayments are shifting and competition isn’t easing. Here’s what’s catching my eye:

- Borrowing activity lifts, but standards hold

- Rates rise as lenders move fast

- Tight rentals meet record prices

- New debt caps reshape loan approvals

Keep reading for all the news.

Call me now on 0402 408944

Monthly Finance Tips - December 25

- Details

With Christmas around the corner, the property and lending landscape is still moving fast. From tightening loan rules to rising prices, here are the key changes that could shape your plans for early 2026

With Christmas around the corner, the property and lending landscape is still moving fast. From tightening loan rules to rising prices, here are the key changes that could shape your plans for early 2026

- Prices rise as listings tighten again

- How new lending caps could change your budget

- Help to Buy scheme gives buyers a new path

- Rising inflation clouds next year’s rate moves

Call me now on: 0402 408944

Koolee Industries Pty Ltd., ACN. 007 748 405, Credit Representative Number 398993

National Mortgage Brokers Pty Ltd., ABN 88 093 874 376, Australian Credit License 391209

Shane Khoo has access to a panel of lenders through National Mortgage Brokers Pty Ltd (ACN 093 874 376 / Australian Credit Licence 391209), which is a fully-owned subsidiary of Liberty Financial Pty Ltd (ACN 077 248 983 / Australian Credit Licence 286596). Shane Khoo has access to products including those from Liberty Financial.