Newsletter | Your Monthly Finance Tips

Monthly Finance Tips - March 2024

- Details

Happy autumn! Hope you’re enjoying the falling leaves and the return of the football codes. Here’s what’s making news in finance and property:

Happy autumn! Hope you’re enjoying the falling leaves and the return of the football codes. Here’s what’s making news in finance and property:

- Investor activity rises

- Stamp duty costs rising

- Conditions improving for FHBs

- New home purchases up 5.3%

Call me now on 0402 408944

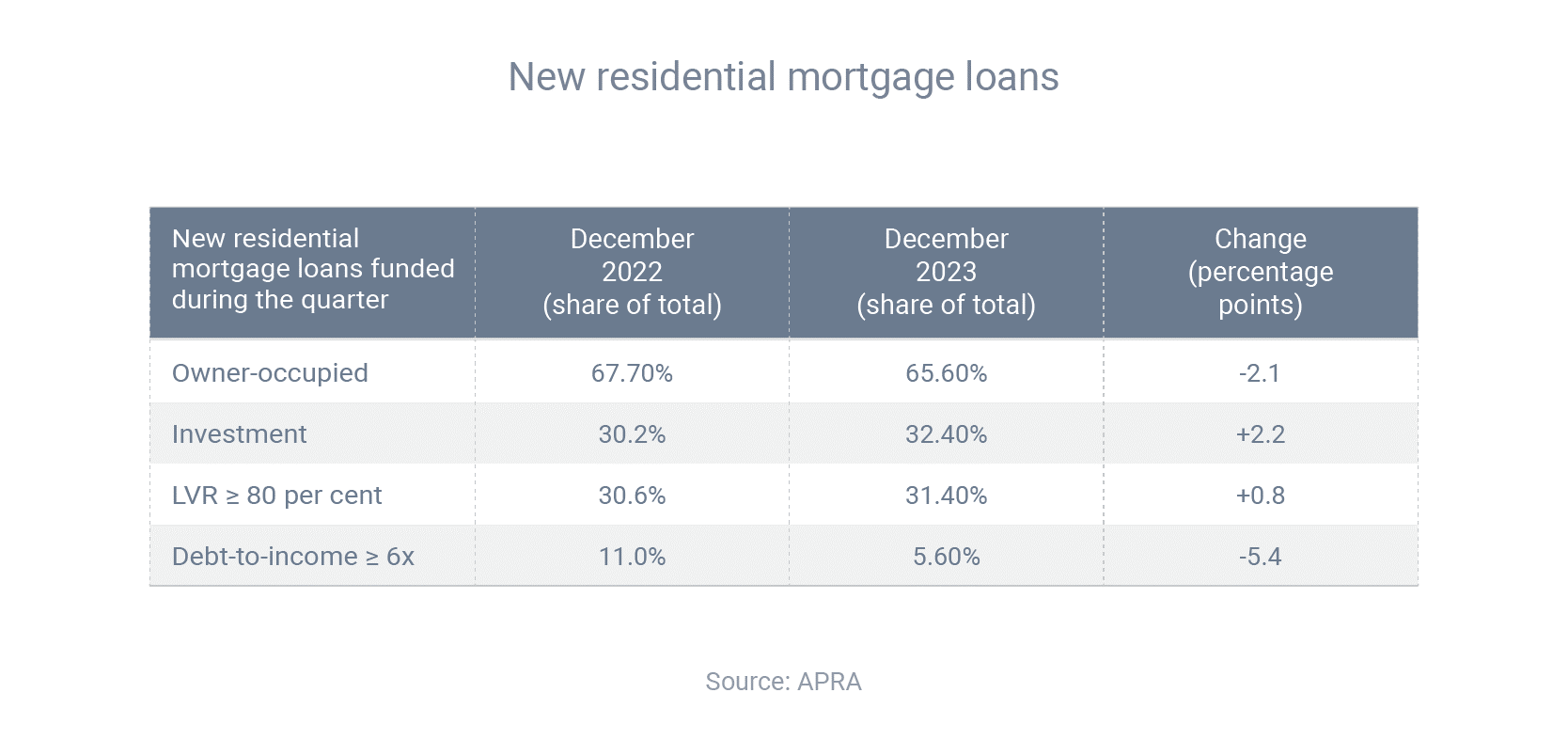

Investor activity rises, high-debt borrowing falls

The latest tranche of home loans data from the banking regulator, APRA, has revealed three interesting shifts in the mortgage market over the past year.

First, there's been a meaningful rise in investor activity during that time. During the December 2022 quarter, 30.2% of new loans were for investment purposes; but in the December 2023 quarter, the share increased to 32.4%. There's been a corresponding decline in owner-occupier activity, which fell from 67.7% to 65.6%.

Second, there's been a sharp decline in borrowing with a debt-to-income of 6 or greater (e.g. someone on a $100,000 salary borrowing $600,000 or more). This fell from a 11.0% share of new loans in December 2022 to only 5.6% in December 2023.

Finally, the share of borrowing with a loan-to-value ratio of 80% or higher has actually increased, from 30.6% of new loans in December 2022 to 31.4% in December 2023.

Stamp duty costs rising due to 'bracket creep'

New research by the e61 Institute and PropTrack has revealed there's been a significant increase in relative stamp duty costs in recent decades.

Back in the early 1980s, buyers in Sydney, Melbourne, Brisbane and Adelaide needed to do about one month's work to cover the cost of stamp duty, assuming they purchased a median-priced property and earned the average post-tax income. But as of 2023, it takes about six months’ work in Sydney and Melbourne, five in Adelaide and four in Brisbane.

Last year, almost all buyers faced a stamp duty rate equivalent to at least 3% of the sale price, while, in the early 1990s, almost all buyers paid less than this amount. PropTrack senior economist Angus Moore said the two reasons stamp duty had become relatively more expensive were because property prices had grown faster than incomes and state governments had allowed ‘bracket creep’ to occur with stamp duty tax brackets.

PropTrack senior economist Angus Moore said the two reasons stamp duty had become relatively more expensive were because property prices had grown faster than incomes and state governments had allowed ‘bracket creep’ to occur with stamp duty tax brackets.

“Bracket creep happens, firstly, because the price brackets have been updated only infrequently and, secondly, because home prices have grown, often substantially, since the brackets were last set,” he said.

“That means more properties have moved up the brackets and are now paying higher rates of stamp duty.”

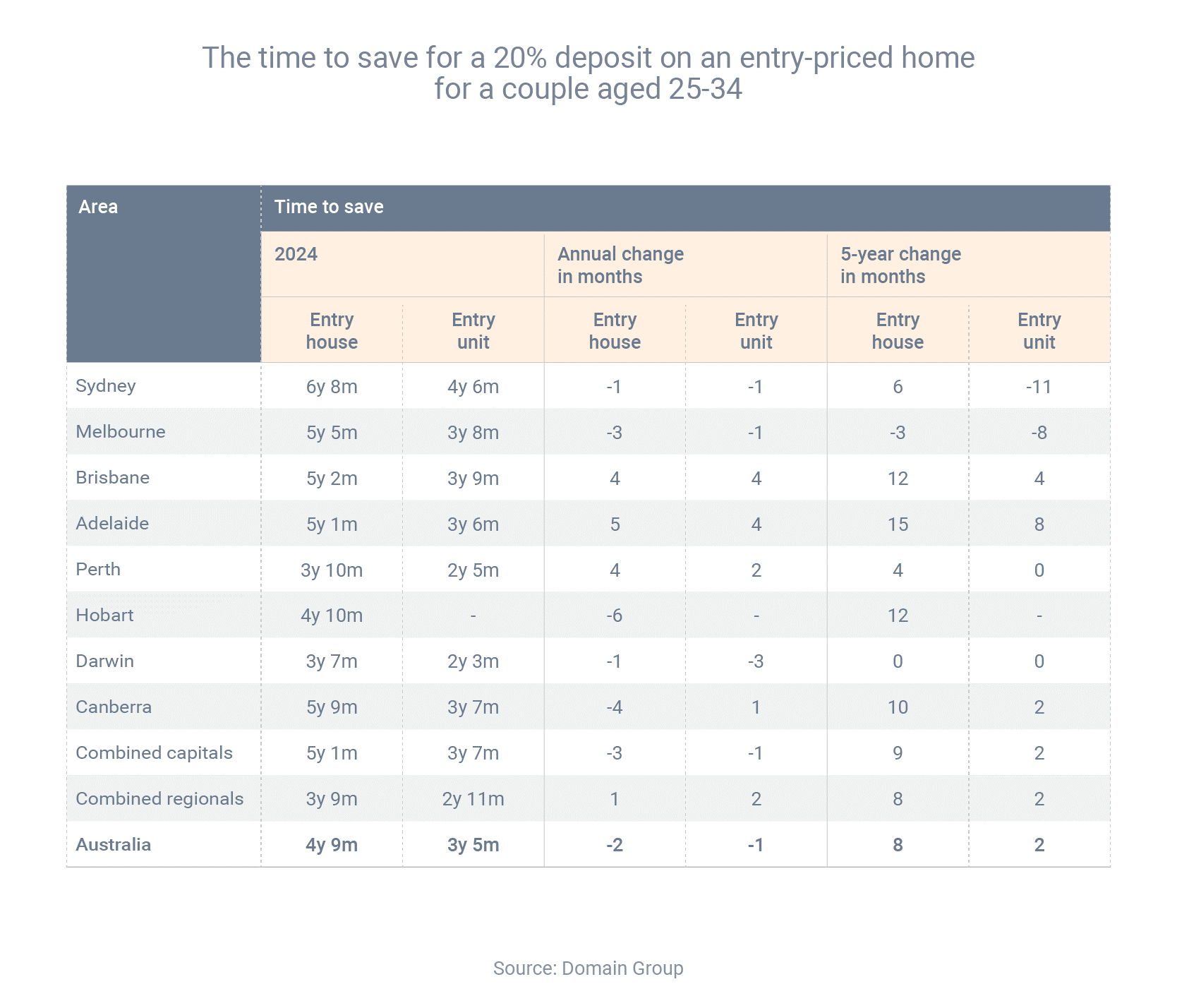

Deposit hurdle gets slightly lower for first home buyers

First home buyers are able to enter the market a little faster than a year ago, new research has found.

At a national level in February, it took 4 years 9 months for a first home buyer to save a 20% deposit on an entry-level house, compared to 4 years 11 months the year before. For an entry-level unit, the time to save a deposit was 3 years 5 months – one month faster than the year before.

Domain classified an entry-level property as one ranked at the 25th price percentile (with the 1st percentile being the cheapest home and the 100th being the dearest). Domain's calculations assumed that first home buyers were a couple aged between 25-34, earning an average salary for someone their age.

The reason that first home buyers are now able to save a deposit more quickly is not because property prices have fallen over the past year – because they've actually increased. Rather, it's because earnings power (through a combination of higher wages and higher savings account interest rates) has grown faster than property prices.

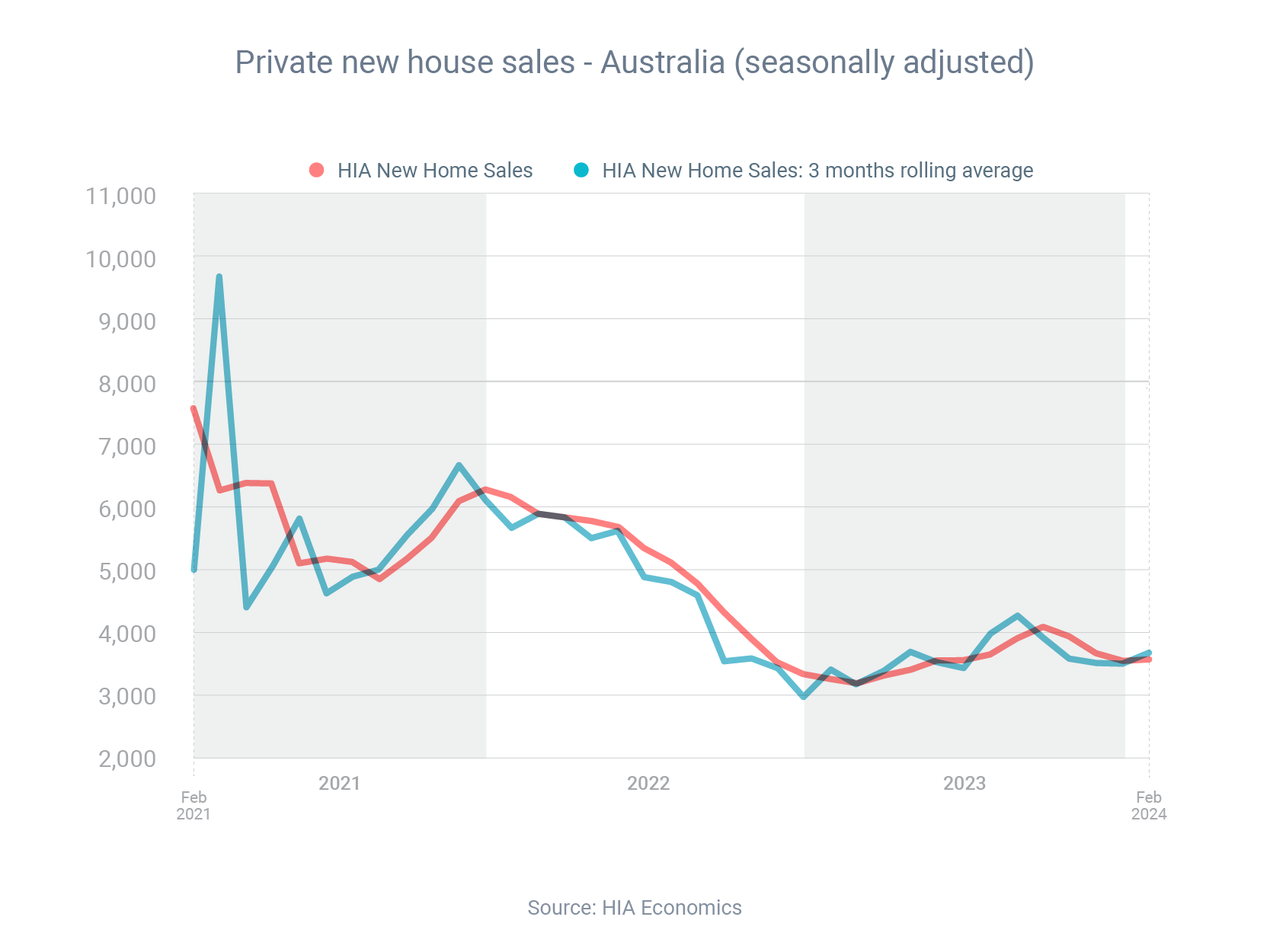

New home purchases rise 5.3%

Australians purchased 5.3% more new homes in February than the month before, according to the Housing Industry Association (HIA).

However, HIA chief economist Tim Reardon said this increase was off a “very low” base. Based on the number of new homes being approved for construction and purchased, he forecast there would be a decade-low amount of homebuilding activity in 2024, despite the pent-up demand for housing.

Nevertheless, banks are still keen to lend to Australians who want to build a new home or renovate an existing one. To finance your project, you’ll need a construction loan (rather than a regular home loan). Here’s how construction loans work:

- To apply for a loan, you need to provide the lender with your building contract, building plans and council approvals

- You receive the money in stages (usually five) throughout the project, rather than one lump sum at the start

- You pay interest only on the portion of the loan you’ve received, not the entire amount

- Construction loans typically have terms of 12-24 months; they may then revert to a standard home loan

Mortgage Broker with over 30 years experience, I can help first home buyers - buy their 1st home, home buyers buy their second, third or fourth home, investment property investors and people who want to build a home.

Based in Victoria Point, I have helped clients all over Australia purchase a home including Gold Coast, Brisbane, Cleveland, Redland Bay, Thornlands, Thorneside, Ormiston, Alexandra Hills, Mt Cotton, Victoria Point, Wellington Point, Birkdale, Shailer Park and the greater Logan area.

Monthly Finance Tips - February 24

- Details

The stories that caught my eye this month cover home loans, lender's mortgage insurance and the property market:

The stories that caught my eye this month cover home loans, lender's mortgage insurance and the property market:

- When should you buy?

- FHB loans rise 12.9%

- 50% of borrowers unsure about LMI

- Rental growth continues

Read more below.

Call me now on: 0402 408944

Monthly Finance Tips - December 23

- Details

Here are some interesting stories about home loans, interest rates and property investing to round out 2023:

Here are some interesting stories about home loans, interest rates and property investing to round out 2023:

- 23% of buyers from interstate

- RBA gives cash rate hint

- Borrowing rises 5.6%

- Credit scores rise

Read more below.

Call me now on: 0402 408944

Monthly Finance Tips - January 24

- Details

I hope you had a lovely Christmas. We’re now a few weeks into 2024 and there’s been plenty of big news:

I hope you had a lovely Christmas. We’re now a few weeks into 2024 and there’s been plenty of big news:

- Investor borrowing up 18%

- Property prices rise 8.1%

- Building approvals rise

- How to be better at money

Read more below.

Call me now on: 0402 408944

Monthly Finance Tips - November 23

- Details

Friendly reminder not to leave your Christmas shopping too late! As we approach the end of the year, here’s what’s happening in the home loans and property markets:

Friendly reminder not to leave your Christmas shopping too late! As we approach the end of the year, here’s what’s happening in the home loans and property markets:

- Home loans activity rises

- Fixed-rate transition continues

- Property market keeps growing

- Bank funding costs increase

Call me now on: 0402 408944

Koolee Industries Pty Ltd., ACN. 007 748 405, Credit Representative Number 398993

National Mortgage Brokers Pty Ltd., ABN 88 093 874 376, Australian Credit License 391209

Shane Khoo has access to a panel of lenders through National Mortgage Brokers Pty Ltd (ACN 093 874 376 / Australian Credit Licence 391209), which is a fully-owned subsidiary of Liberty Financial Pty Ltd (ACN 077 248 983 / Australian Credit Licence 286596). Shane Khoo has access to products including those from Liberty Financial.